Feature ArticleSTARTUP SUPPORT TO BUILD THE FUTURE

The University of Tokyo Edge Capital Partners (UTEC) is known as one of Japan's largest independent venture capital (VC) firms. COO & Managing Partner SAKAMOTO Noriaki, who also serves as general manager of the Planning Department at the Japan Venture Capital Association, shares the insights he gained as a venture capitalist and his take on the current state of startup investment.

Startups are emerging companies aiming for rapid growth through their innovative technologies or business models. They are expected to be a driving force for economic revitalization and restructuring by solving societal issues and creating new industries. Unlike conventional venture businesses that generally seek stable growth over the medium- to long-term, startups aim to rapidly expand their business through venture capital and exit via IPOs or M&A.

Managing Partner, COO and Representative Director

The University of Tokyo Edge Capital Partners Co., Ltd. (UTEC)

SAKAMOTO Noriaki

After graduating from the Faculty of Economics, the University of Tokyo, joined the Ministry of Economy, Trade and Industry (METI). Left METI in 2008, served as vice president of a logistics company, and then earned his MBA from Columbia University. Following work at McKinsey & Company, joined UTEC in August 2014. Is also general manager of the Planning Department, Japan Venture Capital Association (JVCA). Based in Tokyo, he frequently travels abroad to oversee startup investment on the ground.

What is the story behind UTEC’s establishment?

What is the story behind UTEC’s establishment?

UTEC was born in 2004 to expedite the social implementation of university intellectual property and patents as part of the reorganization of national universities into independent administrative corporations. We are informed by how U.S. universities monetize licenses and university startups. While maintaining close ties to the university, we primarily secure private-sector funding. By incorporating private-sector discipline and healthy pressure, UTEC designs incentives for attracting top talent and serves as a bridge connecting the lab to the market.

UTEC was born in 2004 to expedite the social implementation of university intellectual property and patents as part of the reorganization of national universities into independent administrative corporations. We are informed by how U.S. universities monetize licenses and university startups. While maintaining close ties to the university, we primarily secure private-sector funding. By incorporating private-sector discipline and healthy pressure, UTEC designs incentives for attracting top talent and serves as a bridge connecting the lab to the market.

Can you talk about UTEC’s investment track record and key characteristics?

UTEC has invested in about 160 companies, with 20 IPOs and 22 M&A exits. The University of Tokyo biopharmaceutical development startup PeptiDream is a flagship case. Its debut on the then-TSE Mothers in June 2013—opening at 3.2 times the IPO price—was an iconic occasion that boosted momentum for university-affiliated VCs.

Of our six funds, the latest, UTEC 6 Limited Partnership, raised over half of its capital from institutional investors including domestic and foreign pension funds and insurance companies, and sovereign wealth funds. It had its first closure in April 2025, with approximately JPY50 billion. Our total AUM (assets under management) is around JPY130 billion, with about one-third of our investments made overseas. We are successfully balancing independence as a private VC and giving back to academia.

In our first fund, there were a relatively large number of investments for startups in their middle to later (growth to stable) stages. But, beginning from the second fund in 2009, we made a major strategic shift to “seed (pre-launch) × lead (taking a leading position such as providing the largest investment).”

This was driven by the realization that maximum returns come from seed and lead investments. Additionally, investing from the middle stages can easily put us at a disadvantage due to information asymmetry. Becoming deeply involved by taking the lead from an early stage is now UTEC’s standard approach. PeptiDream was also a seed × lead investment, and it generated returns on a scale that could repay the entire fund by itself.

What is the role of a VC?

This can be sorted into four activities: fundraising (raising capital from investors and managing the fund), sourcing (finding and initially evaluating investment candidates), creating value (recruiting, business development, fundraising support, and providing close management support through participation on the board), and exiting (recovering investment through IPOs or M&A).

With “early, deep, and long” as our guiding principles, we take the approach of commitment from start to finish by being involved in management from the seed stage to exiting. An example is our sourcing capability: the many researchers at the University of Tokyo generate some 600 inventions a year. UTEC’s priority access to cutting-edge technologies allows for repeated hypothesis testing from the exploratory phase.

In terms of value-creation, UTEC possesses a recruiter license and over the past seven years, we have introduced over 100 CxO-level executives to portfolio companies. We provide close, practical support from recruitment and organizational development to alliances and board operations. Drawing on these strengths, we offer seamless support from customer profile design to story building, company valuation, and contract processing.

What investment areas are you focusing on?

Our three main areas are semiconductors, robotics, and drug discovery. Regarding semiconductors, Japanese companies still maintain a large presence in equipment, materials, and design tools, with a rich portfolio of research papers and patents. There are also robust research assets in the field of robotics, centered on the University of Tokyo, and through the integration of robotics and AI, we expected nonlinear growth in both software and hardware. For drug discovery, exploration efficiency has soared due to advancements in computational chemistry and measurement technology.

We also see opportunities in “non-rational, passion-driven areas” (where purchase and ongoing use are dictated by human emotions such as fandom, hobbies, and experience value), which are not easily absorbed by general-purpose AI chat user interfaces. Meanwhile, it is highly likely that differentiation will become difficult for SaaS (software as a service), which competes with general-purpose AI in some functions.

What are the challenges facing the domestic ecosystem?

First, a weak statistical foundation. The definition of startups and their data have not been standardized, with discussions tending to be based on feelings. Without clear facts, both policy and support measures can lose focus.

Second, the scarcity of successful large-scale M&A deals. There have been iconic deals in the U.S., such as Google's acquisition of Android and Facebook's acquisition of Instagram, which transformed market behavior.

Meanwhile in Japan, driven by a sense of crisis over sluggish growth, large corporations advanced the establishment of CVC (corporate venture capital) firms. But simply launching CVCs is not enough, and in some cases genuine M&A is necessary to drive business transformation. Only an M&A can connect the new business to the core and change the profit structure. Just one large, high-quality, iconic M&A deal would immediately change the flow. Should that happen, capital will naturally shift to M&A, even in Japan.

What do you keep in mind when investing overseas?

For overseas investments, we do not establish local offices but make frequent business trips to remain deeply involved in our seed × lead investments. Because of the distance, we place importance on preparations and KPI design, enabling high-density decision-making possible with limited face-to-face talks. Governance and information can be sources of concern for Japanese investors looking overseas, but our firm is able to give them peace of mind by securing visibility through attending management meetings and serving as board members.

At UTEC, what we call a “Japan story” is an essential investment condition. This means the investment must satisfy at least one of three criteria: the technology originates in Japan (e.g., fields such as quantum computing where fundamental knowledge from Japan is at the core); it would be meaningful in the Japanese market (e.g., fits structural factors such as Japan’s aging society and healthcare system); or it has partnership potential with Japanese companies (e.g., hardware/software complementation or joint development for sustainable profitability). Even for overseas ventures, we rigorously assess whether “connecting the company to Japan will create nonlinear value.”

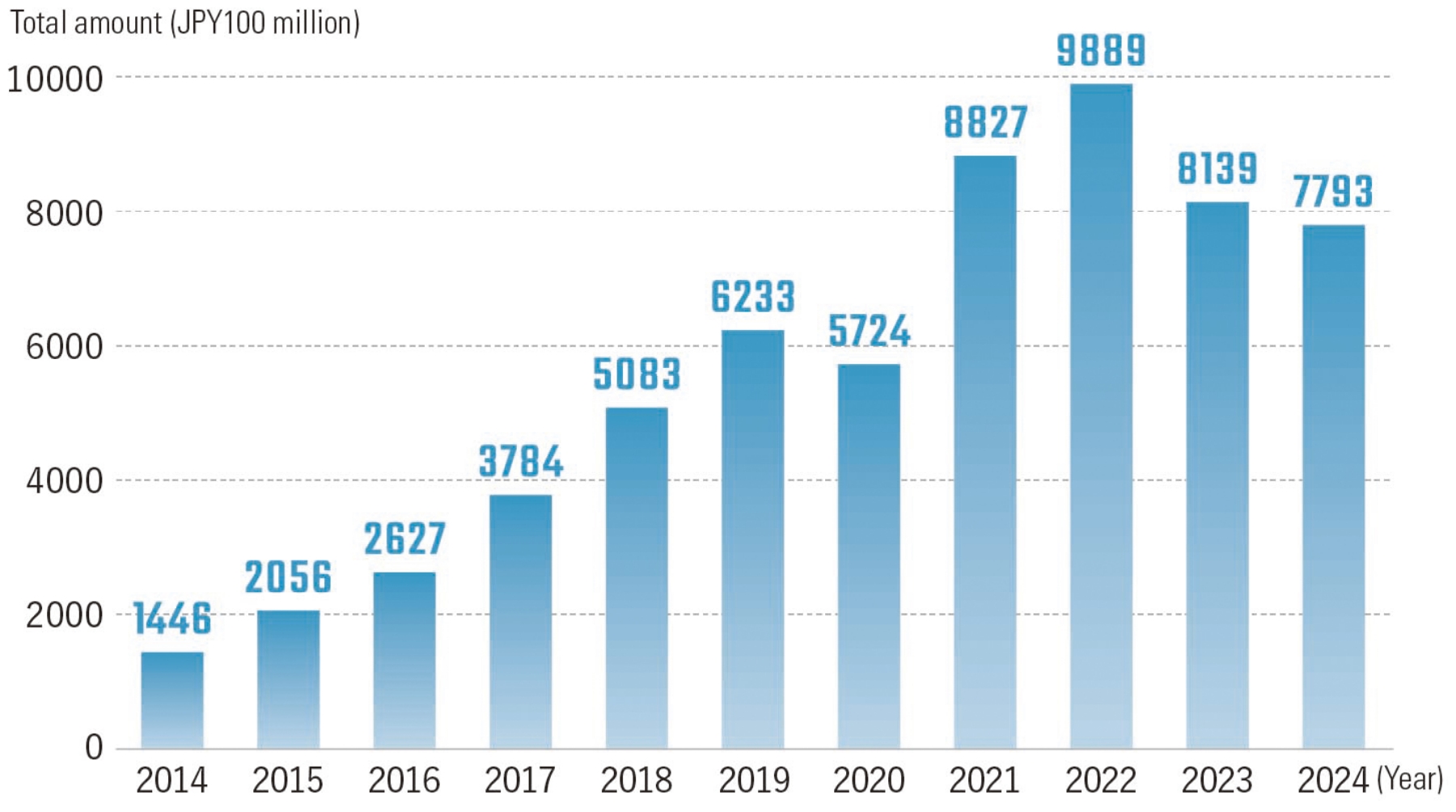

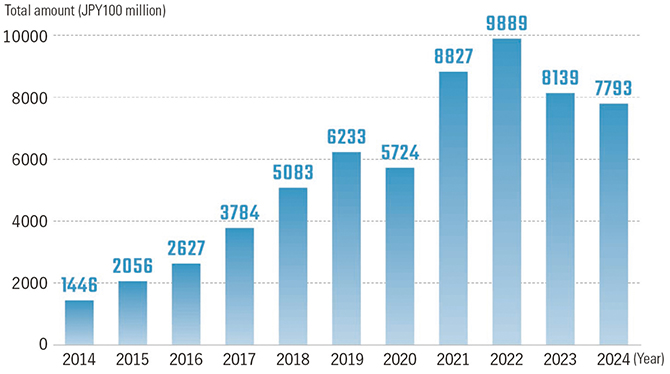

by domestic startups

Although there was some volatility before and after the COVID-19 pandemic, total funding raised by startups is increasing over the medium and long term, growing more than fivefold over the past decade.

Source: “Japan Startup Finance 2024” by Speeda

What is your take on startup investment trends in Japan and globally?

Globally, investments peaked in 2021–22, when the COVID-19 pandemic was having huge impacts, and since then funds have tightened. Massive amounts of capital are currently concentrated in AI-related startups, creating a sort of bubble. Corrections will probably come to this overheated AI bubble, but the technological advancement is irreversible. It would be unwise to avoid it “because it's a bubble.”

Success or failure will depend on distinguishing price from value, and whether nonlinear advantages can be built into product superiority, data superiority or revenue models. In the field of AI, the difference between winners and losers will become increasingly stark.

Circumstances are slightly different in Japan. Investment has increased more than fivefold in 10 years, although a significant share of this was investments by CVCs. There was relatively little decline even during the post-2021 correction period, and median VC returns are competitive. There has also been a recent influx of major overseas VCs to Japan, partially spurred by China risk and the exchange rate conditions.

It is often said that Japan has a small number of unicorns, but this is largely due to structural matters. As the hurdles to going public in Japan are relatively low, many companies list before reaching a valuation of USD1 billion. Since they cannot be defined as unicorns, they are not included in the statistics.

What qualities are needed in an entrepreneur?

Flexibility and the will to view oneself objectively. They also need to make decisions like bringing in professional executives from outside and stepping back from the frontlines, accept dilution of shares, and have the composure to select the optimal exit strategy such as IPO or M&A.

Generally speaking, there is a low success rate for cases where a researcher is the company’s president. The reason why many university startups falter lies in management. While passion for your technology is admirable, it is important for growth to let investors know that they are willing to expand corporate value, even if it means relinquishing some of their shares—ultimately increasing their own returns.

What philosophy does UTEC hold dear?

“Providing support that is almost stifling.” We make a huge commitment from the earliest possible stage, and are consistently involved in everything from human resources to governance, fundraising, and exit strategies. By creating a cycle of funding and talent within academia and building iconic cases of success, we aim to foster a fertile environment where embracing challenges becomes the norm. Centering on Japan's strengths in science and deep tech, while partnering with domestic and international players, our goal is to increase the number of “world-class ventures originating from Japan.” To make sure that happens, we intend to continue providing hands-on support.

UTEC draws on the accomplishments of its VC business to regularly give back to the University of Tokyo and other universities, bolstering support for researchers and students. Its head office is located within the University of Tokyo's South Clinical Research Building (shown above).